In most cases, people do not need to tell HMRC about savings interest because banks and building societies automatically report interest payments to HMRC.

If tax is due, HMRC typically collects it through a tax code adjustment or a Simple Assessment.

However, individuals may need to contact HMRC if their savings and investment income exceeds £10,000, if they complete a Self Assessment tax return, or if taxable interest exceeds their available allowances and HMRC has not made contact.

Interest earned within an ISA remains tax-free and does not count towards the Personal Savings Allowance.

Key Takeaways:

- Most UK banks and building societies report savings interest automatically to HMRC, reducing the reporting burden for taxpayers.

- Basic-rate taxpayers can earn up to £1,000 of interest tax-free via the Personal Savings Allowance, while higher-rate taxpayers get £500, and additional-rate earners receive £0.

- Low-income earners and retirees can stack multiple allowances together to earn up to £18,570 in savings interest completely tax-free.

- Savings and investment income exceeding £10,000 creates a mandatory requirement to register for Self Assessment and file a tax return.

- Tax on interest is usually collected automatically by HMRC through PAYE tax code adjustments or Simple Assessment notices.

- If you owe tax that hasn’t been automatically collected, you must contact HMRC by March 31st following the tax year to avoid penalties.

- Overpaid tax on savings interest can be actively reclaimed using Form R40 within a strict four-year claim window.

- All interest earned inside an ISA remains completely tax-free and does not count toward your Personal Savings Allowance limits.

What Counts as Savings Interest for UK Tax Purposes?

Before determining whether someone needs to notify HMRC, it is important to understand what qualifies as savings interest.

Savings interest refers to income earned from money held in savings accounts, fixed-rate bonds, regular saver accounts, credit union accounts, and certain investment products that generate interest.

Many people assume that only traditional savings accounts count. In reality, HMRC considers interest earned from a wide range of financial products when calculating taxable savings income. The total amount of interest received during a tax year contributes towards a person’s savings income position.

Types of Savings Income HMRC Considers Taxable

HMRC generally considers the following forms of savings income when calculating tax liability:

- Interest from bank and building society savings accounts

- Interest from fixed-term savings bonds and regular saver accounts

- Interest from peer-to-peer (P2P) lending platforms

- Interest from overseas savings accounts

- Interest distributions from Unit Trusts, Investment Trusts, and Open-Ended Investment Companies (OEICs)

- Interest on statutory compensation payouts, such as Payment Protection Insurance (PPI) compensation interest

- Income from life annuity contracts and government/corporate bonds

Interest earned within tax-efficient products such as Individual Savings Accounts (ISAs) is treated differently and remains exempt from income tax.

Does HMRC Automatically Know About Your Savings Interest?

One of the most common concerns among UK savers is whether HMRC can see the interest earned on savings accounts. In most situations, the answer is yes.

Banks and building societies submit information regarding savings interest directly to HMRC. This reporting process means HMRC generally receives information about interest payments without requiring individual taxpayers to submit details separately.

As a result, most people do not need to contact HMRC each year simply because they have earned interest on their savings. Instead, HMRC uses the information provided by financial institutions to determine whether tax is due and how it should be collected.

Martin Lewis has frequently highlighted that many savers mistakenly believe they must manually report every pound of interest they earn. He has explained that financial institutions already provide much of this information directly to HMRC, reducing the reporting burden for most taxpayers.

Source:

https://www.moneysavingexpert.com

When Must Someone Notify HMRC About Savings Interest?

Although automatic reporting covers most situations, certain circumstances require direct action.

Individuals may need to notify HMRC if they are not already completing a Self Assessment tax return and believe taxable savings income has not been correctly accounted for.

Situations involving overseas savings accounts, substantial investment income, or unusually large interest payments may require additional reporting obligations.

Taxpayers should also consider contacting HMRC if they believe information held by HMRC is inaccurate or incomplete.

Situations That Require Direct Action

The following table highlights common situations and the corresponding reporting requirements.

| Situation | Action Required |

| Interest within Personal Savings Allowance | Usually no action required |

| Interest reported by UK banks | Usually no action required |

| Savings and investment income above £10,000 | Register for Self Assessment |

| Overseas savings interest | May require reporting |

| HMRC has not adjusted tax despite taxable interest | Contact HMRC |

| Already filing Self Assessment | Include savings interest on return |

Understanding these exceptions helps taxpayers avoid unnecessary penalties or reporting mistakes.

What Is the Personal Savings Allowance and How Does It Work?

The Personal Savings Allowance (PSA) allows many UK taxpayers to earn a certain amount of savings interest without paying tax.

The allowance depends on an individual’s income tax band. The higher a person’s income, the smaller the available savings allowance becomes.

This allowance was introduced to simplify the taxation of savings income and reduce the number of taxpayers needing to report relatively small amounts of interest.

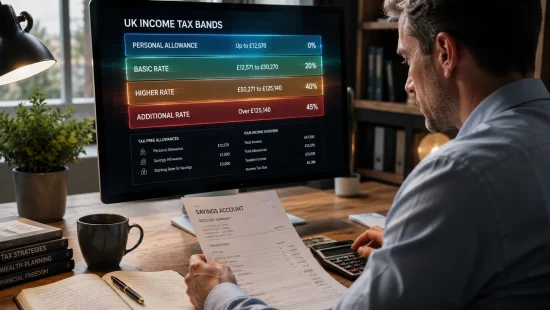

Personal Savings Allowance Thresholds by Tax Band

The following table summarises the current structure of the Personal Savings Allowance.

| Taxpayer Status | Personal Savings Allowance |

| Basic-rate taxpayer | £1,000 |

| Higher-rate taxpayer | £500 |

| Additional-rate taxpayer | £0 |

A basic-rate taxpayer earning £800 in savings interest during the tax year would generally pay no tax on that interest because it falls within the available allowance.

By contrast, an additional-rate taxpayer receives no Personal Savings Allowance and may face tax on all taxable savings interest earned.

What Happens If Savings Interest Exceeds £10,000?

Savings and investment income exceeding £10,000 represents a significant reporting threshold for many taxpayers.

In these circumstances, HMRC generally expects individuals to register for Self Assessment and complete a tax return. This allows HMRC to calculate the correct amount of tax based on the individual’s full income position.

Failure to register when required can potentially lead to penalties, interest charges, or further compliance issues.

Helen Thornley, Technical Officer at the Association of Taxation Technicians, has noted that taxpayers should not assume HMRC will always resolve complex savings income situations automatically. Where reporting obligations exist, timely disclosure remains important to avoid complications.

Source:

https://www.att.org.uk

What Should Someone Do If HMRC Has Not Contacted Them?

There are situations where taxable savings interest exceeds available allowances, yet HMRC has not adjusted a tax code or issued a Simple Assessment.

In such cases, taxpayers should not assume that no tax is due. Instead, it may be sensible to contact HMRC and clarify the position.

Taking proactive action can help prevent future tax bills, interest charges, or penalties arising from underpaid tax.

Although HMRC receives substantial amounts of information from financial institutions, administrative delays or data mismatches can occasionally occur.

Avoiding Penalties and Late Reporting Issues

The following table outlines practical steps individuals can take.

| Situation | Recommended Action |

| Unsure whether tax is due | Review annual interest statements |

| Taxable interest exceeds allowance | Check HMRC records |

| No HMRC contact received | Contact HMRC directly |

| Self Assessment required | Register before deadlines |

| Overseas interest earned | Seek guidance on reporting |

Maintaining records of annual savings interest can make resolving any issues significantly easier.

How Does HMRC Collect Tax on Savings Interest?

For most taxpayers, HMRC does not require direct payment immediately after interest is earned. Instead, tax is often collected through administrative mechanisms designed to spread the cost over time.

Where taxable savings interest exists, HMRC may adjust PAYE tax codes to recover the appropriate amount during the following tax year. Alternatively, a Simple Assessment may be issued where tax remains unpaid and no tax return is required.

Understanding how HMRC collects tax can help taxpayers recognise that receiving a tax code adjustment is often a routine administrative process rather than a sign of wrongdoing.

Tax Code Adjustments

A tax code adjustment is one of the most common ways HMRC collects tax on savings interest. When HMRC receives information from banks and building societies showing that an individual has earned taxable interest above their available allowance, it may alter the person’s PAYE tax code.

This adjustment effectively spreads the tax collection across future salary payments or pension income rather than requiring a separate payment. For many employees and pensioners, this process happens automatically and requires little or no action.

Tax code adjustments are often used where the amount of tax due is relatively straightforward to calculate. HMRC estimates the expected savings interest and incorporates it into the tax code calculation for the following tax year.

Individuals should always review their tax code notices carefully. If the estimated savings interest appears incorrect, contacting HMRC promptly can help avoid underpayments or overpayments of tax.

Simple Assessment Notices

A Simple Assessment is another method HMRC uses to collect tax where a formal Self Assessment return is not required.

Under this system, HMRC calculates the tax due based on information it already holds. The taxpayer receives a notice explaining the amount owed and the deadline for payment.

Simple Assessments are commonly used where HMRC has received savings interest information directly from financial institutions and can determine the tax liability without requiring additional information from the taxpayer.

For many savers, receiving a Simple Assessment is simply part of the normal tax administration process. However, taxpayers should review the figures carefully to ensure they accurately reflect their circumstances.

Is Savings Interest Inside an ISA Taxable?

One of the most attractive features of an Individual Savings Account (ISA) is its favourable tax treatment. Interest earned within an ISA is generally exempt from income tax regardless of the amount earned.

This means ISA interest does not use any portion of the Personal Savings Allowance and does not need to be included when calculating taxable savings income.

For individuals with substantial cash savings, ISAs can provide a valuable way to protect future interest earnings from tax. As interest rates have increased in recent years, many savers have become more aware of the potential tax advantages offered by ISA products.

Why ISA Interest Remains Tax-Free?

The government created ISAs to encourage personal saving and investment. As a result, qualifying interest earned within these accounts remains sheltered from income tax.

The distinction is important because taxpayers may have both taxable and tax-free savings simultaneously. For example, a person could earn interest from a standard savings account while also earning tax-free interest within a Cash ISA.

Understanding this separation can help savers manage their finances more efficiently and potentially reduce future tax liabilities.

Beyond ISAs: Using Spousal Transfers to Reduce Savings Tax

If you have maxed out your annual ISA allowances and face a tax bill on your remaining savings interest, you can legally minimize your liability through asset transfers if you are married or in a civil partnership.

Because HMRC assesses individuals independently, assets can be transferred freely between spouses without triggering capital gains or income tax at the point of transfer.

If one partner is a higher-rate taxpayer (with a £500 PSA) or an additional-rate taxpayer (with a £0 PSA) and the other is a basic-rate or non-taxpayer, moving the savings into the lower-earning spouse’s name allows the household to utilize their larger £1,000 Personal Savings Allowance, Starting Rate for Savings, or unused Personal Allowance.

How Does the Starting Rate for Savings Affect Tax Liability?

The Starting Rate for Savings is often overlooked because many taxpayers are unaware it exists. This special tax rule can provide additional tax-free savings income for individuals with relatively low levels of non-savings income.

Where earned income, pensions, and other non-savings income fall below certain thresholds, taxpayers may qualify for a starting rate band of up to £5,000 for savings income.

The available amount gradually reduces as non-savings income increases. As a result, not everyone qualifies for the full benefit.

Understanding both the Starting Rate for Savings and the Personal Savings Allowance is important because the two reliefs can work together. In some cases, individuals may be able to receive several thousand pounds of savings interest without paying any tax at all.

The Starting Rate for Savings Thresholds

To qualify for the full starting rate, your non-savings income (such as salary or pension) must be less than your Personal Allowance (£12,570) plus the full £5,000 starting rate.

Every £1 of non-savings income above your Personal Allowance reduces your starting rate for savings by £1.

- If your non-savings income is £12,570 or less: You get the full £5,000 starting rate for savings completely tax-free.

- If your non-savings income is £15,000: Your allowance is reduced by £2,430 (£15,000 minus £12,570). Your remaining starting rate for savings is £2,570.

- If your non-savings income is £17,570 or more: Your starting rate for savings drops to £0. However, you can still utilize your standard Personal Savings Allowance (PSA).

Sarah Coles, Head of Personal Finance at Hargreaves Lansdown, has highlighted that many lower-income savers overlook valuable tax-free savings allowances because they focus solely on the Personal Savings Allowance and remain unaware of the Starting Rate for Savings.

Source:

https://www.hl.co.uk

The “Stacking Rule”: How to Earn Up to £18,570 Tax-Free

For low-income earners, retirees, or stay-at-home spouses with minimal personal income, multiple allowances can be stacked together. This strategy allows you to maximize the amount of money you can make from interest before HMRC requires any reporting or tax payments.

If you have no earned non-savings income, your allowances stack as follows:

Allowance Type | Amount Available | Cumulative Tax-Free Total Personal Allowance | £12,570 | £12,570 Starting Rate for Savings | £5,000 | £17,570 Personal Savings Allowance (PSA) | £1,000 | £18,570

Note: If your total income across salary, pensions, and savings combined falls under £18,570, you may owe absolutely no tax on your interest. If your bank has automatically deducted tax or if HMRC has miscalculated your code, you can claim this back directly.

Can Pensioners Be Taxed on Savings Interest?

Pensioners are subject to broadly the same savings interest rules as other taxpayers. The amount of tax due depends on total income, available allowances, and the amount of savings interest earned during the tax year.

Many pensioners benefit from a combination of the Personal Allowance, Personal Savings Allowance, and potentially the Starting Rate for Savings. This means some retirees can earn a significant amount of interest before any tax becomes payable.

However, pensioners with larger pension incomes or substantial savings may still face tax on part of their savings income. The key factor is the individual’s overall tax position rather than age alone.

Retirees should regularly review their annual interest statements and tax notices to ensure HMRC’s calculations remain accurate.

How Can Someone Check Whether They Owe Tax on Savings Interest?

Reviewing potential tax liability starts with understanding how much interest has been earned during the tax year.

Most banks provide annual interest summaries that show the total interest credited to an account. Taxpayers can compare this information with their available allowances to determine whether any taxable amount may exist.

Checking HMRC correspondence, tax code notices, and Personal Tax Account information can also help identify whether savings interest has already been taken into account.

What Does a Real-Life Example of Savings Interest Tax Look Like?

Many taxpayers find practical examples easier to understand than technical guidance. The following examples illustrate how savings tax can work in real-world situations.

Example of a Basic-Rate Taxpayer

Consider an employee earning £30,000 annually who receives £700 in savings interest from a high-interest savings account.

Because the individual is a basic-rate taxpayer and receives a Personal Savings Allowance of £1,000, the entire £700 falls within the allowance. No tax would normally be payable on the savings interest.

In this situation, there would generally be no requirement to notify HMRC solely because the interest was earned.

Example of a Higher-Rate Taxpayer

Now consider an individual earning £65,000 annually who receives £1,200 in savings interest.

As a higher-rate taxpayer, the available Personal Savings Allowance is £500. This means £700 of the interest exceeds the allowance and may be subject to tax.

HMRC may collect the tax through a tax code adjustment, a Simple Assessment, or Self Assessment, depending on the taxpayer’s circumstances.

These examples demonstrate why overall income is such an important factor when determining savings tax liability.

What Steps Should Someone Take If They Think They Have Underpaid Taxes?

Discovering a potential underpayment can be concerning, but taking prompt action is usually the best approach.

The first step is to review savings interest statements and compare them with HMRC records. If a discrepancy appears to exist, contacting HMRC directly can help clarify the position.

Voluntarily disclosing errors often leads to a smoother resolution than waiting for HMRC to identify the issue independently.

Step-by-Step Action Plan & Legal Deadlines

- Check Your Tax Calculation Timeline: HMRC typically issues P800 tax calculations or Simple Assessment letters between June and March following the end of the tax year. If you haven’t received communication but know you owe tax, do not ignore it.

- The March 31st Rule: If your taxable savings interest has exceeded your allowances and it hasn’t been collected automatically via PAYE or a Simple Assessment notice by March 31st following the relevant tax year, you must contact HMRC directly to avoid late-notification penalties.

- Claiming Back Overpaid Tax (Form R40): If you are a non-taxpayer or low earner and your bank or investment fund has mistakenly deducted tax from your interest, do not wait for HMRC. You can actively reclaim this money by submitting Form R40 (Claim a repayment of tax on savings and investments).

- The 4-Year Claim Window: Keep in mind that you have a strict four-year deadline from the end of the tax year in which the tax was overpaid to claim your refund. Claims made outside this window will be rejected by HMRC.

Taxpayers should also retain supporting documentation, including annual bank statements and correspondence relating to savings income.

In more complex cases involving overseas income, multiple savings products, or substantial investment earnings, professional tax advice may be worthwhile.

Conclusion

For most UK savers, the answer to “Do I Have to Notify HMRC of Savings Interest?” is no. Banks and building societies generally report savings interest directly to HMRC, allowing tax to be collected automatically through tax code adjustments or Simple Assessments where necessary.

However, individuals should remain aware of situations requiring action, particularly where savings and investment income exceeds £10,000, overseas interest is involved, or HMRC has not accounted for taxable interest correctly.

Understanding the Personal Savings Allowance, ISA rules, and reporting obligations can help taxpayers remain compliant while making the most of available tax-free savings opportunities.

Frequently Asked Questions

Does savings interest from multiple bank accounts get combined for tax purposes?

Yes. HMRC generally considers the total savings interest earned across all taxable accounts during the tax year. It is the combined figure that is compared against available savings allowances rather than the interest from each account individually.

How often do banks report savings interest to HMRC?

Banks and building societies typically provide savings interest information to HMRC as part of regular reporting processes. The exact timing can vary, but HMRC usually receives sufficient information to assess whether tax is due.

Can HMRC access savings account information automatically?

In most cases, yes. Financial institutions provide relevant savings interest information directly to HMRC, which helps the tax authority calculate liabilities without requiring separate reporting from most taxpayers.

Does joint account interest affect the Personal Savings Allowance?

Yes. Interest from joint accounts is generally divided according to ownership arrangements, often equally between account holders. Each individual then applies their own savings allowances to their share of the interest.

Is tax paid differently on fixed-rate bonds and savings accounts?

The taxation principles are generally similar because both generate savings interest. However, the timing of when interest is credited and reported may differ depending on the product structure.

What happens if a person accidentally fails to report taxable savings interest?

The outcome depends on the circumstances. HMRC may request payment of unpaid tax and, in some situations, charge interest or penalties. Prompt disclosure usually helps resolve matters more effectively.

Does moving money between savings accounts create a tax liability?

No. Simply transferring money between accounts does not normally create a tax charge. Tax considerations generally arise from interest earned rather than movement of funds.

Can someone reduce tax on savings legally through ISAs?

Yes. ISAs remain one of the most popular ways to shelter savings interest from income tax. Interest earned within qualifying ISA accounts is generally tax-free.

Are children’s savings accounts subject to the same tax rules?

Children’s accounts have specific tax considerations, particularly where money is provided by parents. The exact treatment depends on the source of funds and the amount of interest generated.

Does savings interest earned overseas need to be reported to HMRC?

In many cases, yes. UK taxpayers may need to declare overseas savings interest, and the reporting requirements can be more complex than those for UK-based accounts. Professional advice may be beneficial where overseas income is involved.

{

“@context”: “http://schema.org/”,

“@type”: “BlogPosting”,

“mainEntityOfPage”: {

“@type”: “WebPage”,

“@id”: “https://www.bestbusinessblog.co.uk/do-i-have-to-notify-hmrc-of-savings-interest”

},

“author”: {

“@type”: “Person”,

“name”: “David”

},

“publisher”: {

“@type”: “Organization”,

“name”: “Best Business Blog”,

“logo”: {

“@type”: “ImageObject”,

“url”: “https://www.bestbusinessblog.co.uk/wp-content/uploads/2023/07/Best-Business-Blog-Logo7814-300×90.png”

}

},

“headline”: “Tax on Savings Income: Do You Need to Tell HMRC?”,

“image”: “https://www.bestbusinessblog.co.uk/wp-content/uploads/2026/06/Tax-on-Savings-Income-550×310.webp”,

“datePublished”: “2026-06-24”,

“dateModified”: “2026-06-24”

}